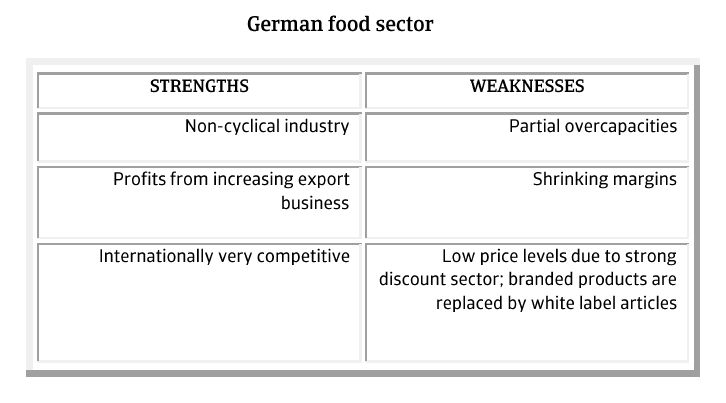

The German food sector has continued to grow in the first half of 2014. Domestically, there is increased competition caused by large retailers and discounters’ dominating market share.

Germany

- Limited direct impact of Russian food ban

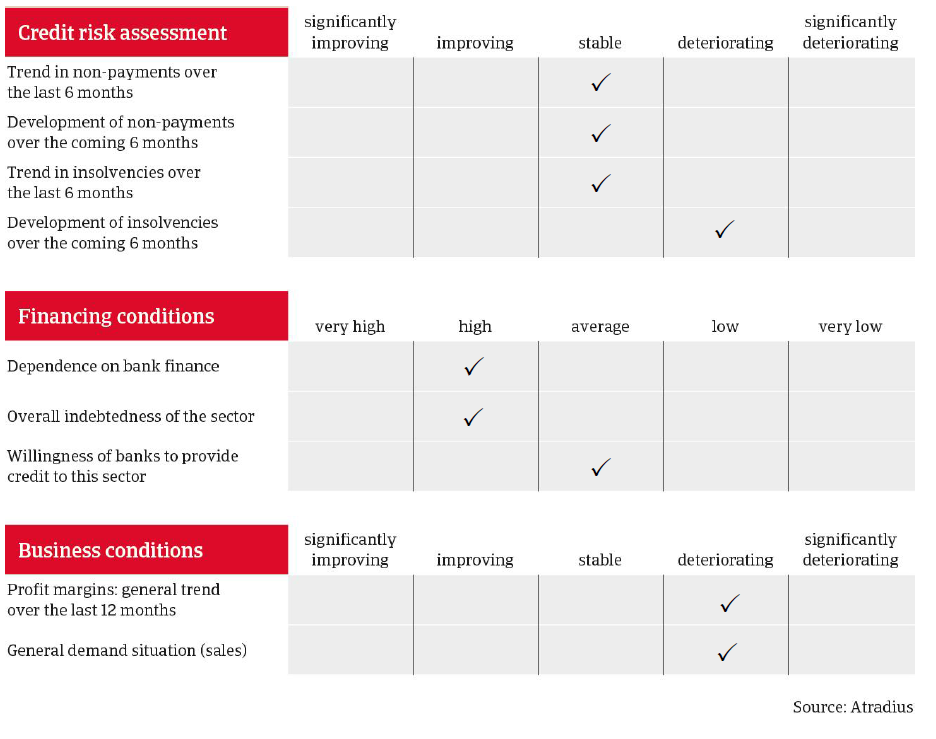

- Slight increase in insolvencies

- An increase in fraud cases

The German food industry continued to grow in the first half of 2014, although slower than in 2013. According to the German Food Association BVE, nominal turnover increased 0.2% year-on-year, to EUR 85.6 billion, with domestic sales rising 0.4%, to EUR 59.7 billion, while export sales fell 0.1%, to EUR 25.9 million. That said, real sales (domestic and export) decreased 0.4% (in 2013: up 1.0%).

Generally, equity strength is good in this sector, but larger groups and producing companies are usually better capitalised than wholesalers or retailers. In terms of solvency and liquidity, larger companies are normally better financed than smaller ones.

Domestically, there is fierce competition in the German food sector because of the market power of the large retailers and discounters that have increased their market share over the last few years. Their overwhelming market power and the tough competition and price wars in the food retail sector mean that food producers, processors and suppliers have found it difficult to pass on increasing costs such as for raw materials and energy. As a result, their profit margins have declined in recent years: especially for those focused on the often non-essential private label products or dependent on just a few powerful retailers. In the last couple of years food discounters in particular have changed their supply practice, reducing the number of suppliers and focusing on a lower number of larger suppliers.

Nevertheless, despite the problems in the industry, many companies in all food subsectors are doing well. The food sector is non-cyclical, and thus less volatile than other industries. Moreover, the sector’s export share has almost doubled since the mid-1990s, providing business opportunities abroad.

There is little direct impact on the sector from the Russian import ban, with only growers and wholesalers of apples and cabbage directly affected. However, there is an indirect consequence as prices are declining because of larger food volumes in the market. This affects fruit & vegetables, dairy and meat. Businesses with strong export orientation are seeking alternative destinations or trying to increase sales to existing export markets such as China.

Meat/meat processing

Meat/meat products are by far the largest subsector, controlled mainly by a few market-leading meat processors who, over recent years, have created essentially fully vertically integrated groups. Besides those large players, there are many mid-sized or small market participants, with only a minor market share, and these are suffering from the volatility of market prices. Increased raw material costs usually cannot be passed on to retailers or consumers, while in case of decreasing raw material prices the meat processing industry faces the challenge of retailers negotiating lower sales prices from them.

Rising demand for meat worldwide has provided business opportunities for the German meat industry, with a boost to the profit margins of those with the largest export share. However, overcapacity in the German meat and meat processing sector means that suppliers of non-essential products and those that do not export are in danger of sooner or later being squeezed out of the market.

Milk/dairy

There were positive developments in 2013 and early 2014, thanks to high milk prices and increasing volumes. But, as milk farmers produced much more than allowed by the current EU milk quota, they will have to pay a fee for that over-production. After the abolition of the quota in 2015, milk production by German farmers and exports are expected to increase.

Fruit & vegetables

The fruit & vegetable subsector is seeing its already low profit margins falling further. Better sales results are often the result of higher prices rather than volumes, as German domestic consumption is stagnating. While this subsector is not particularly export oriented, the Russian embargo is expected to lead to lower prices as a surplus of supply builds up.

Beverages

Despite lower raw material costs for cereals and sugar, sales prices in the German beverage industry (beer, mineral water, soft drinks etc.) remain under pressure because of lower consumption, increasing consumer price sensitivity, overcapacity and discounting.

The German beer sector is facing continuing market concentration and consolidation and changing consumer behaviour. The number of breweries still appears too high and many are too small to be competitive. In an attempt to reverse the industry-wide decline in sales of beer, many German breweries have begun to offer innovative beer-mix drinks with lower alcohol level. However, with many competing products there is less profit to be had from such innovations.

In the fruit juice industry, high and volatile raw material costs are always a problem. The main issue is that consumers are increasingly choosing cheaper products over pure fruit juices, often as a way to reduce their calorie consumption. Smaller fruit juice producers in particular have suffered from difficult market conditions, as they do not have the means to make adequate investment in necessary production facilities. As a result, several companies have been squeezed out of the market by insolvency, takeover or liquidation, and the trend is towards further concentration.

On average, payments in the food industry take around 30 days (in the food retail sector around 45 days). We have not seen any increase in the number of notified non-payments in the last couple of months and expect this to continue.

With food processing companies and retailers demanding longer payment terms from their immediate suppliers to improve their working capital, a wave of longer terms is being created along the whole supply chain. The already low profit margins are in decline and we expect a slight increase in insolvencies in the short term. In the medium term the number of defaults will probably increase further, threatening mainly smaller buyers and those with poor financial strength.

As the food sector is still robust, our underwriting stance remains generally relaxed, although we can usually provide cover on buyers that have operated for less than a year only if they are affiliated to well-established companies or groups. As a rule, we request financial information annually (balance sheet, profit & loss accounts, interim statements, budget figures and liquidity status). If there are signs that a buyer’s finances are deteriorating, we will increase our monitoring, with quarterly reviews and requests for recent reports of payment experience.

This sector has seen considerable fraud cases, and these are on the rise. Therefore we pay close attention to the number of credit limits that are applied for within a short period, especially where the buyers are recently established and where management and/or shareholders have recently changed or the buyer’s business sector does not match with the goods ordered (e.g. a steel company ordering food items).

Related documents

3.45MB PDF